27 January 2020

Credit Card Fraud

As we become adults, you may get a credit card from the card company or your bank and hoping it never happens to you that you become a victim of credit card fraud. Credit card fraud is the most common type of identity theft and can happen at any time. Most importantly, at some point in your adult life, it could happen and you should know what to do if you’re a victim of credit card fraud or in that situation.

Background Info

Credit card fraud is when someone uses your credit card or credit account to make a purchase you didn’t authorize. Every year, millions of Americans become victims of credit card fraud that costs the national economy billions of dollars. Credit Card Fraud can happen in different ways such as if you lose your card or it was stolen, it can be used by someone to make purchases or other transactions, such as withdrawing money from your savings or checking account, either online or in-person. Another way it can happen is that a fraudster can also steal your credit card account number, PIN and security code to make unauthorized transactions, without needing your credit card present.

Even though your credit card is safely in your wallet, it’s important to monitor all your credit card accounts regularly. What you should do if discover that someone has made unauthorized charges on your credit card account, you should:

- Right away contact the credit card company because if you don’t you could be charged with paying more money than you usually do and can be held responsible for $50 of any fraud charges.

- Change your online passwords and PINs to prevent any damage caused by the fraudster.

- Closely monitor your account activity and purchases because this can be especially helpful if you’re not sure how your info was compromised.

- If you notice any fraud on your bank statements then contact your bank immediately.

- Lastly, request a copy of your credit report, there’s often signs of fraud such as new accounts that don’t recognize and will show up on the credit card statement first.

These are the actions or steps to take if you become a victim of credit card fraud.

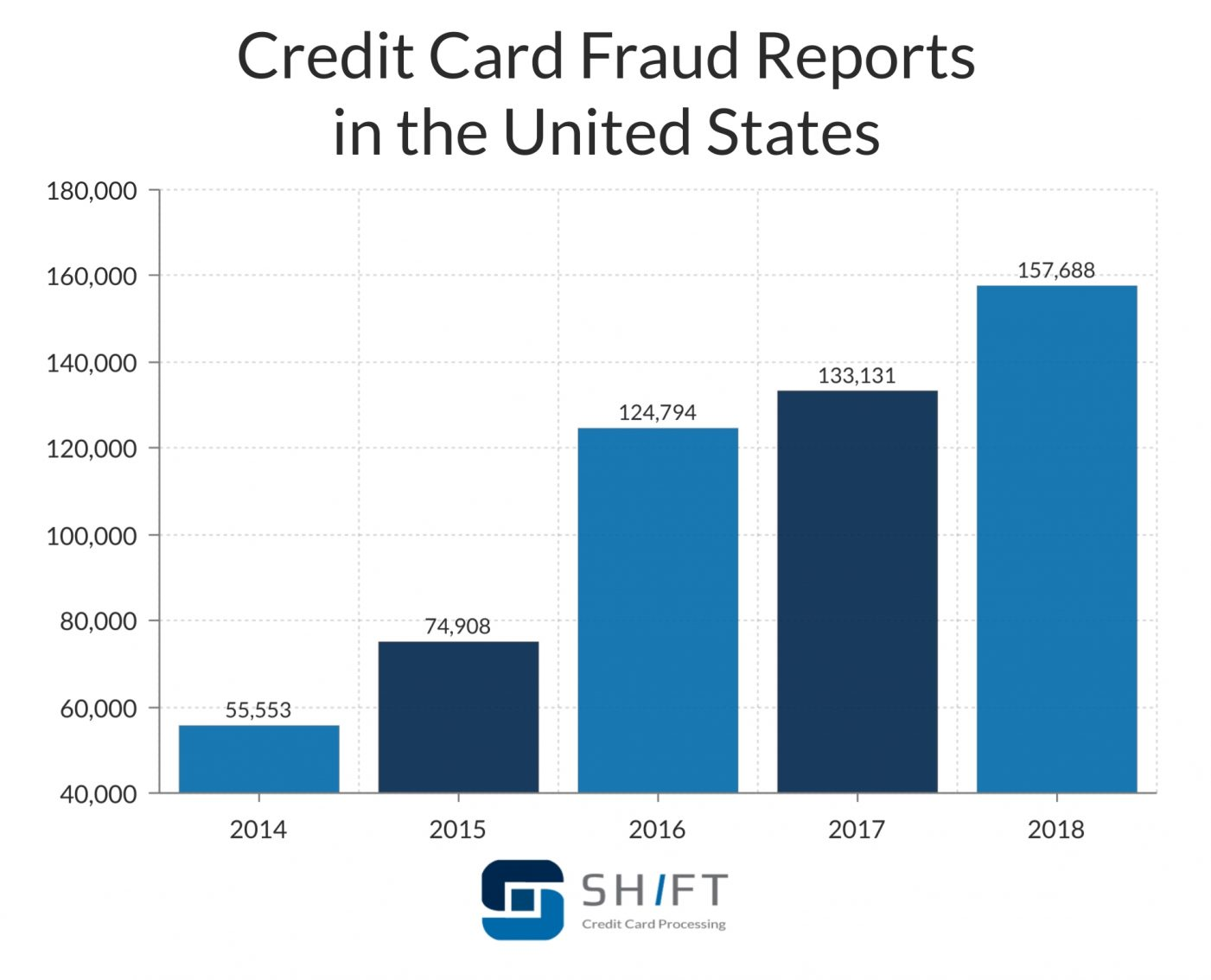

Statistics show that in 2018, $24.26 billion was lost due to payment card fraud worldwide not just in the United States. The United States leads as the most leading country for credit card fraud with 38.6% of cards that were reported stolen or lost by criminals in 2018. In the past 4 to 5 years the graph has increased overtime for the number of credit card fraud reports in the United States and continues to increase over time. Credit Card fraud is the most common and popular kind of identity theft and makes up 35.4% of all identity theft reports. People who are in there ’30s have the highest number of credit card fraud reports which is 40,182. Those are some of the statistics on Credit Card fraud. The most common states California, Georgia, and Nevada for the most on reports of credit card fraud. In Wisconsin, 64 reports per 100k population and the total number of reports in Wisconsin is 3,731.

Credit Card Fraud Punishment

If you were to ask someone what the punishment is for Credit Card fraud it all depends on what state you live in because different states have different laws in prosecuting and classifying it. It can lead to a minor offense meaning you pay a small fine, rarely jail time. A minor offense typically includes stealing the cars but not using it. If it was a misdemeanor, then it’s a combination of a higher fine such as $1,000 or so and sentenced up to one year in the county jail. A misdemeanor in most cases is when the scammer uses a small amount from the stolen credit card such as $500. Now, if it was a felony it would be the most serious crime that often comes with the highest fine ever such as $25,000 and 15 years in prison. So, if you find someone’s card on the ground turn it immediately to the police department and won’t be arrested for Credit Card fraud.

In the future, if you ever become a victim or experienced credit card fraud then you know what to do if it happens and you’re protecting your credit account from your bank or card company and also not paying at least $50 if someone made unauthorized purchases.

Works Cited

Hg.org, www.hg.org/credit-card-fraud.html.“Credit Card Fraud Statistics.” [Updated October 2019] Shift Processing, shiftprocessing.com/credit-card-fraud-statistics/.

“Credit Card Fraud: What to Do If You're a Victim.” Experian, 21 Sept. 2018, www.experian.com/blogs/ask-experian/credit-education/preventing-fraud/credit-card-fraud-what-to-do-if-you-are-a-victim/.

Dukovski, Kliment, et al. “What's the Punishment for Credit Card Fraud?” Finder US, 12 Nov. 2019, www.finder.com/credit-card-fraud-punishment.

“Identity Theft and Credit Card Fraud Statistics for 2019.” The Ascent, www.fool.com/the-ascent/research/identity-theft-credit-card-fraud-statistics/.

There has been a lot of heat about health care and it’s efficiency in the US. From Bernie to Warren to Biden, the topic is numero uno in importance. Why? Well because our system is abysmal compared to other developed countries.

There has been a lot of heat about health care and it’s efficiency in the US. From Bernie to Warren to Biden, the topic is numero uno in importance. Why? Well because our system is abysmal compared to other developed countries.

The French also have a card called carte vitale which identifies you and allows your entire medical history to easily transfer over to different hospitals and doctors. That happens often in France as you get to pick any doctor and none of them can turn you down. The wait times in France is less than the wait time in the US as well which makes a good argument for this system. This system is expensive for global standards but compared to the US it is very cheap. France uses 11% of gdp while US uses 17%. Even though they are paying less their system is ranked better and has better results even with their chronic addiction to cigarettes. This system shows that universal health care can be done well and without a government run system, it provides something Americans are familiar with--choice in insurance funds-- and then provides something Americans can be pleasantly delighted about--complete freedom of choice of doctors.

The French also have a card called carte vitale which identifies you and allows your entire medical history to easily transfer over to different hospitals and doctors. That happens often in France as you get to pick any doctor and none of them can turn you down. The wait times in France is less than the wait time in the US as well which makes a good argument for this system. This system is expensive for global standards but compared to the US it is very cheap. France uses 11% of gdp while US uses 17%. Even though they are paying less their system is ranked better and has better results even with their chronic addiction to cigarettes. This system shows that universal health care can be done well and without a government run system, it provides something Americans are familiar with--choice in insurance funds-- and then provides something Americans can be pleasantly delighted about--complete freedom of choice of doctors.