Title: Which Form of Financial Aid Will Benefit Me Most?

Topic: Financial aid opportunities for prospective college students.

Written by: Kaylie Walters

College is a scary obstacle. Any student, like me, who wants to go to college after highschool is probably terrified of the almost guaranteed debt that’ll come with it. This year, there’s a total of $1.7 trillion in total student debt in the United States, with an average of $37,691 in debt for 45.3 million students studying in America according to educationdata.com.

According to the U.S. News, “About half of current students said student loan debt is making them reconsider finishing college.” This makes me wonder, as a prospective student, is there no way to avoid this debt? What can I do to avoid it? Well, as it turns out, if we’re just a little bit more financially literate and strategic, we can find a way.

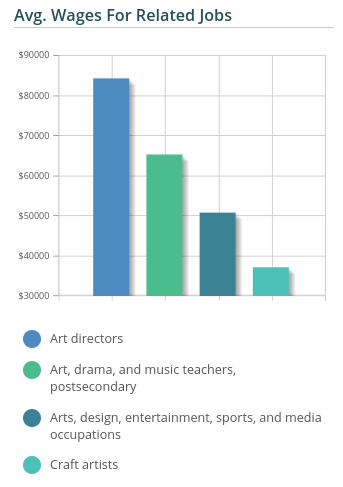

https://thecollegeinvestor.com/21868/financial-aid-award/ (website for image)

Scholarships:

We’ve all heard of scholarships by now, but how much do we really know about it? Scholarships have seemed far out of reach for many students, including me. If you don’t already know, scholarships are a financial aid opportunity you can apply for. Awarded scholarships are typically determined by a student’s demonstrated academic merit. However, there’s a general misconception that only the best students can apply and be awarded with a scholarship. This is not actually true!

There are thousands of scholarships that you can apply for in the United States, so there’s an opportunity for just about anyone. Candidates definitely benefit from having an impressive G.P.A. and academic record, but even those of us who have a 2.0 G.P.A. have the chance to get a scholarship. Scholarships are a free form of financial aid which are awarded by a merit based system which focuses on academic achievements, extracurricular activities, your field of study, etc. According to CNBC, “Each year, more than 1.7 million private scholarships and fellowships are awarded, with a total value of more than $7.4 billion.”

If scholarships are something that interests you, consider looking at scholarships.com to see what scholarships in the United States you may be eligible for, or consider conferencing with your guidance counselor.

https://educationdata.org/financial-aid-statistics (website for diagram)

https://educationdata.org/financial-aid-statistics (website for diagram)

Student Grants (Pell Grants):

Now obviously, not everyone is going to get a scholarship. But there are other options as well: one being student grants. Pell grants are awarded to students who are financially strained, using a student’s E.F.C., or expected family contribution, to judge how much money should be awarded to students who apply. This means that any student of a family who earns $30k or less per year will be eligible to receive a full student grant, with a chance for qualification for some funding with a family income under $60k. Even though 41% of undergraduates each receive an average of $5,179 in federal grants, each year $2 billion in student grants are left unclaimed (out of $32 billion offered) according to educationdata.org. This means that you will have a good chance of receiving a grant, especially since not all of the available grant money is even being used! Student grants are similar to scholarships in that neither require repayment after receiving the donation, as long as the money is used for its intended purpose. Their main differences, though, is that grants have a maximum funding per student of $6,495 (for the 2020-21 school year), and that grants don't strictly base their awards off of student academic achievements like scholarships tend to. So, if your family’s income is $60k or lower, it would likely be worth your time to apply for a grant.

Student Loans:

Student loans are an opportunity which, unlike scholarships and grants, requires repayment of the loaned money, often with considerable interest. Lenders who provide these opportunities often aren’t choosy, which makes it a great opportunity for those who will not be receiving a grant or a scholarship.

https://educationdata.org/student-loan-debt-statistics (website for diagram)

https://educationdata.org/student-loan-debt-statistics (website for diagram)

It is commonly debated whether student loans are a good or bad investment. According to author Paul Sisolak on studentloanhero.com, student loans can very well be both a good and a bad investment, depending on how it is handled. ‘Good debt’ is described as debt that increases in value over time. Take, for comparison, buying a new home over a new car: The home will likely increase in market value over time, while the car will automatically be worth less once you drive it off the lot. The determination of the debt coming from student loans is the same; trying to determine the worth of gaining debt. When considering whether debt is good, consider this: Leslie Tayne, a debt resolution attorney at New York-based Tayne Law Group, described good debt as “a debt that you can easily maintain in your budget and debt that has given you a benefit.” To conclude, when determining whether your debt gained by student loans will be worth it, determine whether the amount of debt is something you will be able to earn back in the near future, and whether the debt is actually benefiting you. Specifically, think about your resolve for college -- will it be worth it?

- - -

There are other forms of financial aid, which are used less often, such as the work-study program. The work-study program offers part-time work for students enrolled in post-secondary education, in which college will pay you for your service. If this interests you, look at what your specific college(s) offers, as every college has different opportunities.

When planning your college debt, it would be most beneficial to apply for both scholarships and grants (if you’re eligible), before applying for a loan. Especially since scholarships and grants can be stacked together without reduction in awarded funds.

I highly recommend applying for FAFSA (Free Application for Federal Student Aid). This is a free opportunity provided to prospective students from the government to see what financial aid opportunities the colleges you are interested in have to offer you. The application for the 2021-2022 school year opened on October 1rst, and it will close on June 30th 2020 -- this is a large gap of time to apply. Be careful, though, as the sooner you apply, the more potential financial aid you may receive.

- - -

In conclusion, It is necessary to consider your current situation when preparing for college when committing to a form of financial aid, as well as college in general. What are your academic achievements thus far? Will you parents be paying for your tuition? And above all, are you sure that college is the route you want to take? Many student grants and scholarships only offer their donations for four to five years, so there is little room for indecision. Student loans will keep adding up as well. “According to the National Center for Education Statistics, just 41% of first-time full-time college students earn a bachelor's degree in four years, and only 59% earn a bachelor's in six years, driving up the cost of attending college significantly.” This may be a clear indicator of why so many students experience as much debt as they do, so make sure you don’t fall into the same trend, whichever path you choose to take.

https://www.petersons.com/blog/the-financial-aid-effect-on-early-decision-and-early-application/ (website for image)

Work Cited:

AbigailJHess. “Graduating in 4 Years or Less Helps Keep College Costs down-but Just 41% of Students Do.” CNBC, CNBC, 20 June 2019, www.cnbc.com/2019/06/19/just-41percent-of-college-students-graduate-in-four-years.html#:~:text=According%20to%20the%20National%20Center,cost%20of%20attending%20college%20significantly.

Bustamante, Jaleesa. “Student Loan Debt Statistics [2021]: Average + Total Debt.” EducationData, 11 Feb. 2021, educationdata.org/student-loan-debt-statistics.

Federal Student Aid, studentaid.gov/understand-aid/types/work-study.

Hanson, Mel. “Financial Aid Statistics [2021]: Average Aid per Student.” EducationData, 6 Feb. 2021, educationdata.org/financial-aid-statistics.

Nadworny, Elissa, and Lauren Migaki. “FAFSA Applications Are Open. Here's How To Fill It Out This Year.” NPR, NPR, 22 Oct. 2020, www.npr.org/2020/10/20/925739424/fafsa-applications-are-open-heres-how-to-fill-it-out-this-year.

Scholarships.com. “Academic Scholarships and Merit Scholarships.” Scholarships for College Free College Scholarship Search 2020-2021, www.scholarships.com/financial-aid/college-scholarships/scholarships-by-type/academic-scholarships-and-merit-scholarships/.

Sisolak, Paul. “Are Student Loans Bad or Good Debt? Here's What You Need to Know.” Student Loan Hero, 27 Nov. 2020, studentloanhero.com/featured/student-loan-debt-good-bad/.

“Student Loan Expectations: Myth vs. Reality.” U.S. News & World Report, U.S. News & World Report, www.usnews.com/news/blogs/data-mine/2014/10/07/student-loan-expectations-myth-vs-reality#:~:text=The%20standard%20repayment%20plan%20for,is%20forgiven%20after%2020%20years.